Accounting Ratios-What are some of the key accounting ratios for evaluating a company’s financial performance? What formulas are used to calculate them?

Accounting ratios analysis is a popular way to figure out a company’s strengths and flaws.

It helps the organisation to determine the relationship between one accounting variable and another on their financial accounts, as well as measure efficiency and profitability.

It can be used to determine the link between statistics on a balance sheet, profit and loss statement, and other financial statements.

What is Finance? Definition & Types of Finance

Accounting Ratios Types

The following are some of the most essential accounting ratios for determining a company’s financial performance:

How to Write a Self-Assessment

1. Liquidity Ratios

Liquidity ratios, often known as Balance Sheet ratios, are subdivided into the following categories:

Ratio of Today

Cash-to-Quick Ratio (Q/C)

Any liquidity ratio’s main purpose is to identify a company’s short-term solvency position. It reflects the company’s efficiency and ability to pay off current liabilities and debts with current assets.

These accounting ratios have the following formula:

Current Assets / Current Liabilities = Current Ratio

Current Assets – Inventory / Current Liabilities = Quick Ratio

Cash Ratio = Current Liabilities / Cash + Marketable Securities

2. Ratios of Profitability

Profitability Ratios are used to evaluate a company’s ability and efficiency in generating revenue and, eventually, profits with its capital.

It is commonly represented in percentage terms and indicates the unit’s relationship in terms of % of sales.

In accounting, there are four different types of profitability ratios:

(Gross Profit / Net Sales) x 100 Equals Gross Profit Ratio

(Net Profit / Net Sales) x 100 Equals Net Profit Ratio

((Cost of Goods Sold + Operating Expense) / Net Sales) x 100 = Operating Expense Ratio

(Profit before Interest and Taxes / Capital Employed) x 100 = Return on Capital Employed

3. Ratios of Activity

Activity Ratios are used to assess a company’s ability to manage and convert its assets into cash and revenue. It displays the company’s ability to generate income through asset leveraging.

In accounting, there are four different types of activity ratios:

Inventory Turnover Ratio: This metric measures how long it takes to convert inventory into sales.

Debtors Turnover Ratio: This ratio measures how quickly credit debtors are converted into cash.

Total Assets Turnover Ratio: This metric measures how well a corporation manages its assets to generate revenue.

Fixed Assets Turnover Ratio: This metric measures how well a company manages its fixed assets to produce revenue.

The accounting formulas for these ratios are as follows:

Inventory Turnover Ratio = Cost of Goods Sold / Average Inventory

Debtors Turnover = Net Sales / Average Debtors

Total Assets Turnover = Sales / Average Total Assets

Fixed Assets Turnover = Sales / Average Fixed Assets

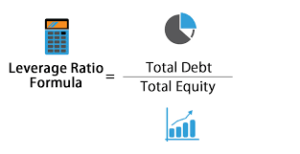

4. Leverage Ratios

The leverage ratio, which comes in four different varieties, is used to estimate the company’s long-term solvency.

Debt to Equity Ratio: This is the proportion of a company’s total indebtedness to its total equity. A low debt-to-equity ratio, which is used to assess a company’s leverage capacity, usually implies that it is financially stable.

Debt Ratio: The relationship between a company’s total obligations and total assets is described by this ratio.

Proprietary Ratio: This figure depicts how the company’s total shareholder funds are allocated among its total assets.

These accounting leverage ratios are calculated using the following formulas:

Total Debt / Total Equity = Debt Equity Ratio

Total Liabilities / Total Capital = Debt Ratio

Shareholders’ Funds / Total Assets = Proprietary Ratio

What are the Benefits of Knowing Accounting Ratios?

Accounting ratios are used to evaluate a company’s performance and determine whether it is stable and able to effectively utilise its assets.

It’s also utilised to foresee and plan for the future, especially in terms of providing information for decision-making.

Accounting ratios are used not only to evaluate a company’s internal performance, but also to compare it to those of other companies in similar industries.

Understanding these accounting statistics as an investor might help you better grasp a company’s prospects.

Jurnal is an accounting software that can assist you in learning more about these topics. Ratios

Jurnal is an online accounting software that offers a variety of functions to help you manage your business finances, including financial reporting, inventory, transaction reconciliation, and tracking purchase invoices and payments.

Because business financial data is appropriately processed in this small business accounting software, you may save money, time, and energy by using the Jurnal by Mekari.

Request a free 14-day trial or contact us for more information.

Ratio Analysis’ Advantages

When used correctly, ratio analysis illuminates many of the company’s issues while also highlighting certain strengths. Whistleblowers are usually ratios, which show management’s awareness of problems that need to be addressed. The following are some of the advantages of accounting ratios:

Ratio analysis will help to confirm or deny the company’s investment, finance, and operational decisions. They break down the financial report into comparable data, allowing management to better analyse and appraise the company’s financial situation and the results of their decisions.

It breaks down complex accounting records and financial data into easy-to-understand statistics of operating performance, financial performance, solvency, and long-term circumstances, among other things.

Ratio analysis aids in the recognition of problem states and draws management’s attention to such measurements. Some data is lost in the complexities of financial accounts, and ratios will help to uncover these issues.

Allows the corporation to handle inter-firm comparisons, business standards, and intra-firm linkages, among other things. This will help the organisation have a better understanding of its financial situation in the economy.

Accounting Ratio Checklist/Requirements

The following are some prerequisites for understanding accounting ratios:

To determine which parts of the business demand more attention.

To gain a better understanding of the prospective regions that can be developed by putting in effort in the desired direction.

Furthermore, to conduct a more thorough examination of the company’s profitability, liquidity, efficiency, and solvency.

It should also provide information for getting cross-sectional studies by assessing performance against the best business standards; and to provide information derived from financial reports that is useful for developing future estimates and measures.

Accounting Ratios’ Limitations

While ratios are extremely useful tools for financial analysis, they do have some drawbacks, such as:

To develop their ratios, the corporation can make some year-end additions to its financial records.

Inflationary price fluctuations are ignored by ratios. Several ratios are calculated based on historical expenses, and they take into account variations in output levels over time. This does not accurately reflect the current financial condition.

Accounting ratios effectively overlook the firm’s qualitative characteristics. They take into account the economical concerns (quantitative).

As a result, different formulas for the ratios may be used by different companies. One example is the current ratio, where some organisations consider all current obligations while ignoring bank overdrafts from current liabilities when calculating the current ratio.

Finally, accounting ratios do not help a corporation solve its financial problems.